What Are Recurring Payments? Meaning, Types, Examples, and How They Work

Identity Verification for Bank Accounts, Credit Cards and Loans

Author:

Aaron Klein

Identity verification confirms that an applicant is the person behind a bank account, credit card application or loan application. U.S. banks, card issuers and lenders use this check before account opening, card approval or loan review. You will see which data they request, why review delays happen and how to protect personal data during digital onboarding.

Contents

- What identity verification means in U.S. financial services

- Why banks, card issuers and lenders verify identity

- What information and documents banks may request

- How online identity verification works?

- How verification differs for bank accounts, credit cards and loans

- Digital vs. in-branch identity verification

- Common identity verification methods

- Why identity verification can delay or reject an application

- How to protect personal data during identity verification?

- Technology behind modern identity verification

- Identity verification regulations and standards in the U.S. and beyond

- Key challenges with identity verification

- Practical example: opening an account, applying for a card and getting an online loan

- What to check before submitting identity documents

- Sources

Identity verification is the process used by financial institutions to confirm that an applicant is the person they claim to be before opening an account, issuing a card, approving credit or allowing a sensitive financial action. The check can include government-issued ID, SSN or TIN, address, phone or email, selfie, document scan, bank account verification, online loan identity verification, KYC, AML, CIP and fraud screening.

What identity verification means in U.S. financial services

Identity verification in banking confirms a person’s legal identity before a financial institution opens a bank account, reviews a credit card request or evaluates a loan application. A consumer signup verifies basic account access. A financial application verifies who controls money, credit and repayment risk.

A bank, credit card issuer or lender checks whether the applicant uses a matching legal name, date of birth, address and identification number. This customer verification connects customer identity to a risk profile, sanctions signals and new account fraud controls. In plain terms, bank identity verification is not just a screen that asks who You are. It is identity proofing tied to financial services, KYC, AML and application review.

The difference is easier to see in a short table:

| Consumer signup | Financial identity verification |

|---|---|

| Confirms basic account access | Confirms legal identity |

| Uses email or phone for account access | Uses ID, SSN or TIN and address |

| Carries low regulatory burden | Connects to KYC, AML, CIP and fraud checks |

| Creates lower financial risk | Creates account, credit, loan and payment risk |

Why banks, card issuers and lenders verify identity

Weak verification lets stolen identities become accounts, loans and payment access inside U.S. financial services. Banks, card issuers and lenders verify identity because one bad match can create fraud, money laundering exposure, unauthorized access and reputational harm. Bank identity verification also gives the institution evidence for regulatory compliance and gives customers a safer path into credit and payments.

The core jobs are:

- Reduce fraud and unauthorized access

- Support regulatory compliance

- Protect customers and account data

- Reduce failed payments and ACH returns

- Maintain customer trust in financial services

Fraud prevention and unauthorized access

Criminals use stolen identities to open fraudulent accounts, connect ACH payments and request loans they do not plan to repay. That is why fraud prevention starts before money moves. A stolen ID can pass a weak signup screen, but proper account verification checks whether the applicant data, bank account details and access path fit the same person.

The risk is not limited to a fake profile. Identity fraud can lead to account takeover, payment fraud, unpaid loans, ACH returns and laundering through accounts that look clean at opening.

| Risk | What verification checks |

|---|---|

| Stolen ID | Whether applicant data matches identity records |

| Fraudulent account | Whether applicant controls the identity and account |

| Payment fraud | Whether account details and access are valid |

| ACH returns | Whether routing and account numbers are correct |

| Loan fraud | Whether borrower identity is real before approval |

Compliance with KYC, AML and CIP rules

KYC requires identity verification, AML requires customer risk assessment and CIP requires identifying data before a bank builds a customer relationship. A bank cannot treat a financial application like a social media login because money movement creates legal duties. Customer identity verification gives the institution a record of who applied, which data was checked and why the application moved forward or went to review.

For a consumer, this explains the extra friction. Financial institutions check customer due diligence, sanctions screening, politically exposed persons, suspicious activity signals and audit trails. Banks maintain CIP records for at least five years. Nacha also governs the ACH network, so account verification supports payment evidence when ACH transfers are involved.

| Framework | What it adds to verification |

|---|---|

| KYC | Confirms customer identity |

| AML | Assesses financial crime risk |

| CIP | Requires identifying data and verification records |

| CDD | Reviews customer profile and expected activity |

| EDD | Adds checks for higher-risk customers |

| Nacha / ACH | Supports payment network verification and audit trails |

Customer trust and financial access

Fraud causes money loss and confidence loss, while excessive checks can block legitimate customers from financial access. Banks need a middle path. Weak verification lets fraudsters enter the system. Overly strict verification can push real applicants into false declines, especially when a person lacks traditional documents or has data that differs across records.

Secure onboarding matters because customers feel the result directly. A delayed account opening, blocked payment or rejected application changes how they judge the bank. Balanced identity checks protect account data, preserve customer trust and still leave room for legitimate applicants who need manual review instead of automatic rejection.

| Verification level | Result |

|---|---|

| Too weak | Fraud, account abuse, unauthorized access |

| Too strict | False declines, exclusion, abandoned applications |

| Balanced | Security, compliance and access for legitimate users |

Better conversion and customer experience

Faster account connection increases completed onboarding and payment completion when the verification path still controls fraud risk. Digital onboarding fails when a user reaches a confusing document step, waits for unclear review or cannot connect a bank account. That friction creates customer abandonment.

Instant account verification improves conversion because it reduces waiting and manual entry. Vendor case studies in the source files tie faster verification to conversion gains, but the published article should cite the original provider claim before using a percentage.

⚠️ Editor note

|

|

|---|---|

|

|

What information and documents banks may request

Banks collect full legal name, date of birth, residential address and SSN or Tax ID to connect an applicant to a real identity record before account opening, card review or a loan decision. Bank verification documents are not one fixed package. A checking account focuses on identity and address. A credit card application ties identity to credit risk. A loan application adds borrower profile, income source and account purpose.

During bank identity verification, a financial institution uses enough data points to match You with official records, reduce false matches and build a risk assessment. Not every product requires the full list, but the bank, card issuer or lender needs the same core result. The applicant, document and financial profile must point to the same legal identity.

The documents and data can include:

- Full legal name

- Date of birth

- Residential address

- SSN, ITIN or Tax ID

- Phone number and email

- Driver’s license, passport or other government-issued ID

- Proof of address

- Employment or income information

- Intended use of the account or loan

How online identity verification works?

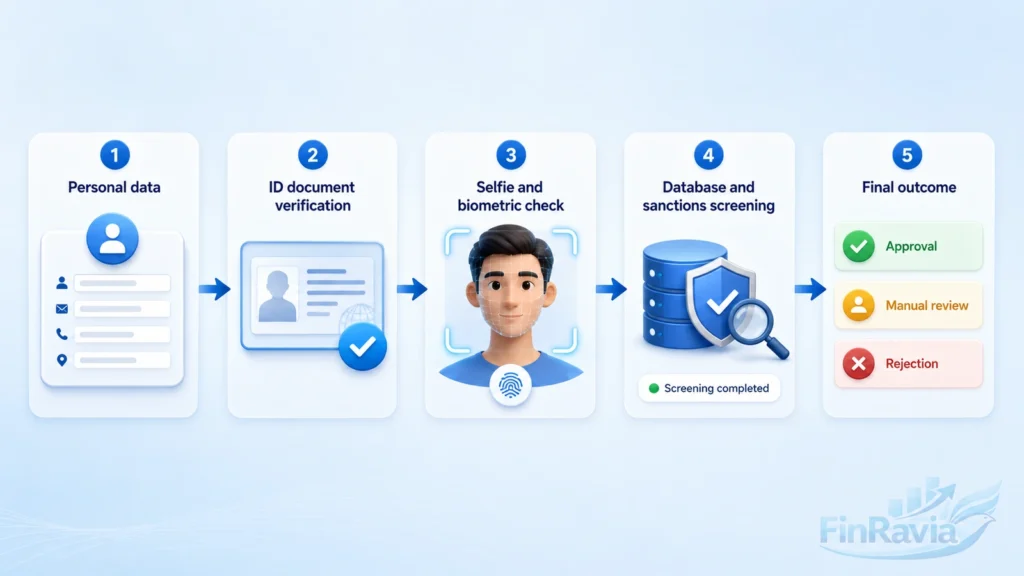

An applicant submits personal data, and a bank system turns it into a five-step bank identity verification process for digital onboarding and online loan identity verification. The path starts with customer data collection, moves through ID document and selfie checks, then reaches database screening, risk assessment and an approval decision.

The flow is:

- Customer data collection

- Identity document verification

- Selfie, biometric verification and liveness check

- Database, sanctions and risk screening

- Approval, manual review or rejection

Step 1 — Customer data collection

Banks collect personal details because name and email do not prove customer identity for a financial account, card or loan. Customer data collection connects full legal name, date of birth, address, SSN or Tax ID with contact details, employment, income sources and intended account use. The bank or lender matches that data against authoritative databases, public documents and internal risk rules before the next verification step.

Step 2 — Identity document verification

A customer uploads a government-issued ID, and OCR extracts document information for comparison with the application data. Identity document verification checks a passport, driver’s license or ID card for document authenticity, expiry date, layout, fonts, security elements and issuing authority signals. AI and authenticity algorithms turn those signals into an authenticity score.

Document-only verification has a clear limit. High-quality fakes make a scanned ID weaker without selfie and liveness checks. That is why the bank identity verification process connects document data to the applicant’s face and risk profile.

| Document signal | What it validates |

|---|---|

| Name and DOB | Applicant data consistency |

| Expiry date | Document validity |

| Watermarks and holograms | Physical authenticity |

| Font and layout | Template consistency |

| Machine-readable zone | Document structure |

| Issuing authority check | Official record match |

Step 3 — Selfie, biometric verification and facial comparison

The customer takes a selfie, and the bank system compares that image with the ID photo to confirm the same person is present. Biometric verification uses a facial image or short video, then facial comparison checks whether the selfie matches the passport photo, driver’s license photo or ID card photo.

The system can convert facial features into biometric data. A faceprint or feature vector represents nodal points, eye position, facial structure and other measurable features. Facial comparison is not the same as facial recognition. For bank onboarding, the practical task is narrower. The bank needs a match between the applicant and the authenticated ID image.

Selfie capture → facial analysis → feature vector or faceprint → ID image comparison → match or no match

| Term | Meaning |

|---|---|

| Facial comparison | Compares selfie with ID photo |

| Facial recognition | Broader technology for identifying or recognizing faces |

| Feature vector | Numerical representation of facial features |

Step 4 — Liveness detection

Liveness detection confirms physical presence and blocks a photo, replayed video, face mask or deepfake from passing as the customer. Active liveness checks ask for movement, such as a blink, smile, head turn or closer camera position. Passive liveness analyzes skin texture, eye movement, depth perception, micro-expressions and light reflections without adding a visible task.

Advanced 3D recognition and thermal imaging add stronger spoof detection, but both require specialist hardware. For consumer onboarding, banks need liveness checks that work through a phone camera while still catching static-photo and replay attacks.

| Liveness method | What it checks | Limitation |

|---|---|---|

| Blink, smile or head movement | Live response | Requires user action |

| Passive liveness | Texture, depth and reflections | Depends on system quality |

| 3D recognition | Advanced spoof detection | Specialist hardware |

| Thermal imaging | Heat and live presence | Not common for consumer onboarding |

Step 5 — Database, sanctions and risk screening

Banks cross-reference customer information with databases, sanctions lists and credit bureau data before the final approval decision. Database checks can include government registries, credit bureaus, phone verification, address verification, sanctions screening, OFAC lists, PEP databases, watchlists and adverse media.

This step matters for credit cards and loans because credit bureau checks show financial history and fraud patterns. It also matters for bank accounts because sanctions screening and risk assessment can move an applicant into enhanced due diligence. The result is not only pass or fail. The system routes the application by risk level.

| Risk level | Verification result |

|---|---|

| Low risk | Approve |

| Medium risk | Additional verification |

| High risk | Manual review or rejection |

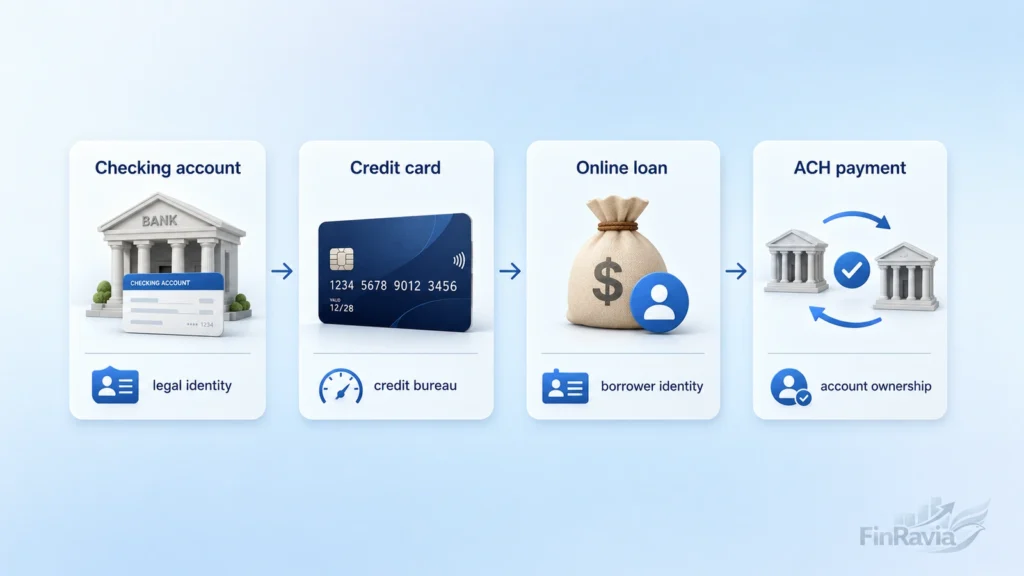

How verification differs for bank accounts, credit cards and loans

Banks verify identity before account opening, card issuers check credit applications and lenders confirm borrower identity before loan approval. The same person can face different checks because each product creates a different financial risk. A bank account gives access to deposits and payments. A credit card creates credit exposure. A loan adds borrower identity, repayment risk and credit file review. Bank verification changes again when an ACH transfer or linked account is involved because account verification must confirm access to a specific bank account.

The comparison is:

| Product | Main verification focus |

|---|---|

| Bank account | Legal identity and account opening |

| Credit card | Applicant identity, credit file and fraud signals |

| Online loan | Borrower identity, loan application and repayment risk |

| ACH account | Account ownership, routing data and transfer access |

Bank account opening

A user opens a new bank account, and the mobile banking app verifies legal identity before access to checking or savings features. The app collects SSN or Tax ID, address and a government-issued ID such as a driver’s license or passport. Selfie verification or biometric comparison links the document to the applicant. KYC then connects the person, document and account purpose.

The core checks are:

- Government-issued ID

- SSN or Tax ID

- Address

- Selfie or biometric comparison

- KYC check

Credit card applications

A card issuer verifies applicant identity before it connects a credit card application to a credit bureau file. The review checks whether name, SSN and address point to the same person. Credit bureau data shows financial history, while fraud patterns show whether the application needs manual review.

The card review is:

| Check | Why it matters |

|---|---|

| Name, SSN and address | Confirms applicant identity |

| Credit bureau data | Shows financial history |

| Fraud patterns | Flags suspicious applications |

| Manual review | Handles mismatches or risk |

Online loan identity verification

Identity verification is used when applying for a loan because a lender must confirm borrower identity before loan approval. Stolen identity and synthetic identity can pass weak checks, create a credit history and lead to loan losses. Online loan identity verification connects the borrower, credit bureau checks, application data and fraud risk before funds move.

I treat loan identity checks as a risk control, not a formality. Application fraud can combine stolen identity data, synthetic profiles and credit-file signals.

Bank account verification for ACH payments and transfers

Bank account verification confirms legitimate access to a bank account and checks routing number and account number data before payment activity. This is different from proving who You are. It proves whether You control the account or action. For a new payee, a banking app can add 2FA, OTP, fingerprint or facial recognition. Tools such as Plaid Auth belong to this account verification layer, while Nacha rules shape ACH payment evidence.

The payment layer is:

| Scenario | Verification focus |

|---|---|

| ACH payment | Account and routing details |

| Account linking | User access to bank account |

| New payee transfer | Step-up authentication |

| Payroll or funding | Account ownership and validity |

| RTP | Fast account detail validation |

Digital vs. in-branch identity verification

In-branch identity verification requires a branch visit, while digital identity verification moves the same identity check into a mobile app or secure browser. In a branch, a bank employee examines original documents, compares Your face with the ID photo, scans records and collects signatures. In bank online identity verification, You photograph an ID, take a selfie and let the digital verification system compare faces, screen databases and create an audit trail.

Digital checks reduce customer effort and can finish in minutes or seconds. Branch checks add human judgment for complex files. A hybrid approach keeps digital first, then sends a high-risk customer to manual review, video verification or a branch when the system needs stronger evidence.

| Factor | Digital verification | In-branch verification |

|---|---|---|

| Speed | Minutes or seconds | Slower |

| Customer effort | App or browser | Travel and wait |

| Document check | Photo, video and automated validation | Original document inspection |

| Human judgment | Lower unless manual review | Higher |

| Scalability | High | Limited |

| Cost at scale | Lower | Higher |

| Fraud risk | Deepfakes, stolen IDs | Fake documents, human error |

| Best for | Remote onboarding | Complex or high-risk cases |

| Audit trail | Strong digital logs | Physical records and scans |

| Hybrid use | Digital first, branch if needed | Branch as fallback |

Common identity verification methods

Banks use multiple identity verification methods because one check cannot cover documents, biometrics, account access and post-opening risk at the same time. Bank identity verification methods online combine document verification, biometric verification, database checks, KBA, OTP, micro-deposits, risk scoring and ongoing monitoring. Together, these layers reduce false approvals and send unclear cases to manual review.

The method map is:

| Method | Main role |

|---|---|

| Document verification | Confirms ID document authenticity |

| Biometric verification | Links person to ID photo |

| KBA / OTP | Confirms knowledge or contact control |

| Account verification | Confirms bank account access |

| Ongoing monitoring | Tracks risk after account opening |

Document-based verification

Document-based identity verification checks a government-issued document before a bank accepts the applicant’s identity claim. A passport, driver’s license or ID card gives the bank a familiar, low-friction source of legal identity. The limit is clear. High-quality fakes weaken document-only review, so the document works best with biometric or database checks.

Authenticity markers include:

- Embedded chips

- Watermarks

- UV-reactive features

- Holographic overlays

- Machine-readable zones

- Font and layout consistency

Biometric and liveness verification

Biometric identity verification adds a second trust layer by comparing a selfie with the ID photo and testing live presence. Facial comparison links the applicant to the document. Liveness detection protects against deepfakes, spoofing and pre-recorded video. AI algorithms check facial structure, micro-expressions, skin texture and light reflections.

| Liveness type | What it checks |

|---|---|

| Active liveness | Blink, smile or head movement |

| Passive liveness | Texture, depth and reflections |

KBA, OTP and trusted identity networks

KBA generates out-of-wallet questions from a credit file, while OTP verification checks control of a phone number or email. A trusted identity network uses existing credentials to reduce onboarding friction. These customer authentication methods help when the bank needs an extra signal beyond an ID document or selfie.

| Method | What it proves | Weak point |

|---|---|---|

| KBA | Knowledge tied to credit file | Hard for some users |

| OTP | Control of phone or email | Contact channel can be compromised |

| Trusted identity network | Existing trusted credentials | Depends on network coverage |

Bank account verification methods

Instant account verification lets users link checking or savings accounts in seconds, while micro-deposits add a slower fallback path. Database validation checks account and routing numbers without a direct live bank connection. Automated micro-deposits verify an account through a small deposit, often over Same Day ACH rails. Manual micro-deposits support edge cases, business accounts and smaller banks.

I treat provider speed claims as useful context, not universal timing. Source files cite under 7 seconds, 12,000+ institutions, 1,900 added U.S. institutions, 75% instant micro-deposit support and 100% manual ACH availability.

| Method | Typical speed from files | Best use |

|---|---|---|

| Instant account verification | Under 7 seconds or seconds | Fast account linking |

| Database validation | Fast, no direct bank connection | Account and routing check |

| Automated micro-deposits | 1–2 business days | Fallback when instant verification is unavailable |

| Manual micro-deposits | 1–2 business days or more | Edge cases, business accounts, smaller banks |

Ongoing monitoring and re-verification

Ongoing identity verification continues after account opening because customer risk levels change over time. Banks monitor behavior, update customer information and use transaction monitoring systems to flag suspicious patterns. A customer can appear on a sanctions list, become a politically exposed person or reactivate a dormant account that later shows fraud risk. Periodic re-verification can happen every year or two.

| Trigger | Why bank re-checks identity |

|---|---|

| Sudden large deposits | Activity differs from profile |

| Rapid fund movement | Possible fraud or laundering pattern |

| High-risk countries | AML risk |

| Dormant account reactivation | Account misuse risk |

| Sanctions or PEP status change | Compliance risk |

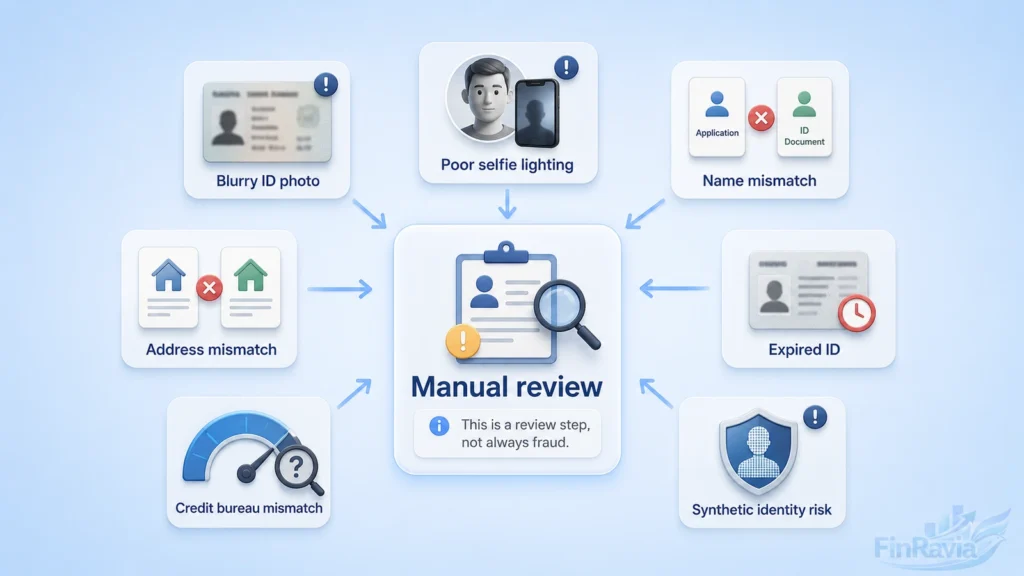

Why identity verification can delay or reject an application

False positives create friction for legitimate applicants when a bank system treats a real person as a risk signal. A failed identity verification result does not always mean fraud. It can come from poor lighting, a damaged document, a name mismatch, database inconsistency, a credit freeze, outdated credit bureau data or a fraud system that sends the file to manual review.

In a bank identity verification process, the applicant, ID document, address, credit bureau record and government database must point to the same identity. Online loan identity verification adds borrower risk and repayment exposure, so the lender reads mismatches more carefully. A rejected application happens when the institution cannot connect the person, document and risk profile with enough confidence.

The main delay points are:

| Signal | Why it delays review |

|---|---|

| Poor lighting | Face match or document scan fails |

| Damaged document | ID data cannot be trusted |

| Name mismatch | Legal name does not match records |

| Database inconsistency | Bank data and external records conflict |

| Credit freeze | Credit file access is restricted |

| Synthetic identity signal | Fraud system sees fabricated identity risk |

Common reasons identity verification fails

Poor lighting causes facial recognition failure because the bank system cannot compare a selfie with the ID photo clearly. A blurry image creates document read failure. A folded, damaged or expired ID can stop bank verification because the document no longer gives a clean identity signal.

Name mismatch creates another path to manual review. Initials, name changes, spelling differences and address mismatch can break the link between the applicant and identity verification documents. Outdated credit bureau data and government database errors create the same problem from the records side. Strict systems can reject real customers when one data point does not fit the rest of the profile.

A failed check often leads to another upload, additional proof or manual review instead of a final denial.

| Problem | What it can cause | What You should expect |

|---|---|---|

| Blurry ID photo | Document read failure | Re-upload request |

| Expired ID | Verification stop | New ID required |

| Name mismatch | Manual review | Additional proof |

| Address mismatch | Delay | Proof of address |

| Poor selfie lighting | Face match failure | New selfie or video |

| Outdated database data | False positive | Manual review |

Synthetic identity and high-risk fraud checks

Synthetic identity fraud combines real information with fabricated data, so a lender can see a profile that looks real at first pass. Fraudsters can combine valid SSNs with fake names, fake addresses and manufactured credit histories. Those profiles can pass basic checks, then create online loan fraud, credit card application fraud and unpaid debt.

Synthetic identities create more friction for legitimate borrowers because fraud patterns force banks and lenders to ask for stronger evidence. Deepfakes and stolen biometric data add another layer of risk. A loan file, card application or account opening can move to manual review when the fraud system sees identity fraud signals across documents, credit history or application data.

I treat synthetic identity checks as a borrower protection issue as well as a lender risk issue. Weak review lets fraud losses enter the credit system, and strict review must still separate fraudsters from real applicants.

What to do if verification is delayed

Complex cases can take several days because manual review handles mismatches, risk signals and additional verification. The result can be approval, extra checks or rejection. The bank or lender asks for more evidence when the system cannot connect the applicant, document, address, phone, email or credit record with enough confidence.

Use the delay to fix the exact weak signal:

- Re-check spelling of Your legal name and address.

- Re-upload a clear ID image if requested.

- Provide proof of address when the bank asks for it.

- Complete phone, email or OTP verification.

- Visit a branch when the institution requires in-person verification.

How to protect personal data during identity verification?

Bank data is shared through identity verification only when user consent connects the applicant, the secure platform and the financial institution. The sensitive information in bank verification can include SSN, Tax ID, address, phone, email, ID document, selfie, video and bank account data. Each item serves a specific check, not a general request for personal data.

A secure platform protects that data through encryption, controlled data handling and access controls. Those controls restrict who can see account data, which third-party provider receives it and how the verification result returns to the bank or lender. Phishing risk starts when a request breaks that structure. A legitimate flow explains the financial action, uses phone verification or email verification when needed and ties the request to account opening, loan review, ACH verification or another clear purpose.

The data types fit these checks:

| Data type | Why it is requested |

|---|---|

| SSN or Tax ID | Identity and financial record match |

| Government-issued ID | Legal identity confirmation |

| Selfie or video | Match person to ID |

| Phone or email | OTP or contact verification |

| Bank account data | Account ownership or ACH verification |

| Address | Identity and proof-of-residence checks |

Technology behind modern identity verification

Technology transformed identity verification from manual document review into an automated system where OCR extracts ID data, AI detects altered text and API checks return database signals in seconds. In modern identity verification, the bank does not rely on one screen or one document. It connects document verification, liveness detection, database connectivity, behavioral biometrics and risk scoring engines into one decision path.

OCR converts a photo of a passport, driver’s license or ID card into structured fields. AI and machine learning compare those fields with document templates, spot inconsistent fonts, detect altered text and flag fraud signals. Liveness detection blocks static photos, replayed videos, masks and deepfake attempts. APIs connect the bank system with databases, account data, sanctions sources and credit checks, which supports real-time verification.

Risk-based analytics decide what happens next. Low-risk applications move toward instant approval, medium-risk files receive added checks and high-risk files go to manual review. Behavioral biometrics add a device-level signal by reading typing rhythm, phone handling and swiping behavior. Cloud infrastructure lets the system handle more verification volume without turning every case into a branch review. Blockchain and DLT belong to the early-stage decentralized identity layer, not the core consumer flow.

The technology stack is:

| Technology | Role in verification |

|---|---|

| OCR | Extracts ID data |

| AI / ML | Detects altered documents and fraud signals |

| Liveness detection | Blocks photo, video and deepfake spoofing |

| APIs | Connect databases and account data |

| Risk scoring | Routes applications by risk level |

| Behavioral biometrics | Flags unusual device or user behavior |

| Cloud infrastructure | Scales verification volume |

Identity verification regulations and standards in the U.S. and beyond

U.S. banks follow CIP because the Customer Identification Program requires a reasonable belief about customer identity before a banking relationship moves forward. In practice, identity verification regulations connect account opening to the Bank Secrecy Act, the Patriot Act, FinCEN, KYC and AML controls.

CIP became a Patriot Act requirement in 2003. Banks keep key CIP records for at least five years, so identity checks create evidence, not just an approval screen. Suspicious activity, sanctions signals and customer due diligence can move a file into deeper review.

The U.S. is the main framework for this article. FATF, AMLD, 5AMLD, 6AMLD, AML5, eIDAS, PCMLTFA and FINTRAC show how other markets connect identity checks to financial crime controls.

The regulatory map is:

| Region | Framework | What it covers |

|---|---|---|

| U.S. | CIP / BSA / Patriot Act / FinCEN | Customer identity in banking |

| Global | FATF | Risk-based customer due diligence |

| EU | AMLD / AML5 / eIDAS | AML, digital ID, electronic signature |

| Canada | PCMLTFA / FINTRAC | Identity verification for financial transactions |

Key challenges with identity verification

Identity fraud constantly evolves, and banks respond with tighter checks that create identity verification challenges for real customers. Deepfakes, forged documents, stolen biometric data and synthetic identity force stronger liveness checks, database checks and manual review. That pressure explains why two banks can give You different experiences for the same account, card or loan application.

False positives frustrate legitimate customers when a fraud system flags a real person. Legacy systems slow digital verification because old bank infrastructure was not built for mobile ID scans, selfies and API screening. Data quality adds another problem. Government databases and credit bureaus can contain errors, outdated credit bureau data or address records that no longer match the applicant.

Strict requirements also create financial inclusion risk. Immigrants, refugees, young people and customers without traditional documents face more friction. Verification cost shapes the final experience too. A bank can apply heavier checks to high-risk cases, while low-value accounts receive a narrower review path.

The challenge map is:

| Challenge | Example | User impact |

|---|---|---|

| Deepfakes | Fake selfie or video | More liveness checks |

| Synthetic identity | Real SSN plus fake profile | More risk review |

| False positives | Real user flagged | Delay or manual review |

| Data quality | Outdated credit or address data | Mismatch |

| Legacy systems | Old bank infrastructure | Slower process |

| Inclusion risk | No traditional documents | More friction |

| Cost | Premium checks vs low-value accounts | Different bank experiences |

Practical example: opening an account, applying for a card and getting an online loan

An applicant opens a checking account, and the bank requests an ID document, SSN, address and selfie before the account access decision. The same person then submits a credit card application, where the card issuer connects identity data with credit bureau signals. For online loan identity verification, the lender checks borrower identity, fraud signals and credit history before the approval decision.

This identity verification example shows why one user can pass bank account opening, then face manual review for a credit card or loan. The document, selfie, SSN and credit file must support the same applicant.

| Product | What may be checked | Possible outcome |

|---|---|---|

| Checking account | ID, SSN, address, selfie | Opened, pending review or rejected |

| Credit card | Identity data and credit bureau signals | Approved, pending or declined |

| Online loan | Borrower identity, fraud signals, credit history | Approved, extra review or rejected |

| ACH payment | Account and routing numbers, account access | Linked, pending micro-deposit or failed |

What to check before submitting identity documents

A clear ID image reduces document read failure before online verification starts. Check that Your identity verification documents show a valid ID, matching legal name and current address. A folded or damaged document, glare, poor lighting or cropped photo can turn a real applicant into a failed verification case.

Bank verification documents also need contact consistency. Your phone number and email must be accessible because phone or email verification can support OTP checks. Address mismatch creates delay when the bank needs proof of address. Name mismatch sends the file to manual review when records, documents and application data do not align.

Before submitting, check:

- Use Your current legal name

- Check address consistency

- Use a valid, readable ID

- Avoid glare and poor lighting

- Keep the document uncropped

- Make sure phone and email are accessible

- Prepare proof of address if asked

Sources

- eCFR — 31 CFR 1020.220 Customer Identification Program for banks

- FinCEN — USA PATRIOT Act

- OCC — final rule on Customer Identification Programs for banks

- FDIC — collecting identifying information under the CIP Rule

- FFIEC — BSA/AML Manual Customer Identification Program

- CFPB — checklist for opening a bank or credit union account

- CFPB — Personal Financial Data Rights rulemaking

- Federal Register — Required Rulemaking on Personal Financial Data Rights

- Nacha — Account Validation Resource Center

- Nacha — account validation FAQs

- NIST — SP 800-63A identity proofing guidelines

- NIST — IAL2 remote identity proofing implementation resources

- NIST — FRTE 1:1 face verification evaluation

- FTC — credit freezes and fraud alerts

- FTC — IdentityTheft.gov recovery resource

- CFPB — summary of rights under the Fair Credit Reporting Act

- CFPB — Equal Credit Opportunity Act and Regulation B

- FATF — global AML/CFT standards body

- European Commission — European Digital Identity

- European Commission — European Digital Identity Regulation

- FINTRAC — methods to verify the identity of persons and entities

- Plaid — bank account verification guide

- Plaid — Identity Verification documentation

- Stripe — bank account verification 101

Frequently asked questions

What is identity verification in banking?

Identity verification in banking confirms customer identity before a bank gives access to financial services. Bank identity verification connects applicant data with legal identity, fraud prevention, KYC and AML compliance, and customer risk assessment, so the institution knows who enters the financial relationship.

Why do banks need identity verification?

Banks need identity verification to confirm legal identity before money, credit or payment access moves forward. The check supports KYC, AML and fraud prevention because a bank account, card or loan can be misused for unauthorized access, identity theft or financial crime.

What documents are required for bank verification?

Bank identity verification documents connect the applicant to legal identity, address and financial records. A bank can request a government-issued ID, proof of address, SSN or Tax ID, phone and email checks, legal name, date of birth and address. Higher-risk products add employment, income or account-purpose information.

How does online loan identity verification work?

Online loan identity verification confirms borrower identity before the lender makes a loan approval decision. The lender checks ID data, SSN or Tax ID, address, credit bureau information, fraud signals and borrower records. Some applications add selfie verification or document verification when risk signals require stronger evidence.

How long does identity verification take?

Identity verification time depends on the verification method and the risk level of the application. Instant bank account verification can finish in seconds. Automated micro-deposits take one to two business days. Manual review and complex risk checks can take several days when records, documents or fraud signals do not align.

What is the difference between identity verification and bank account verification?

Identity verification confirms who the applicant is, while bank account verification confirms account ownership and account validity. A bank uses identity verification for legal identity, KYC and fraud screening. Account verification checks whether a person or business controls a specific account, routing number and payment access.

What is the difference between instant verification and micro-deposits?

Instant verification confirms account access through digital account connection or database checks, while micro-deposits confirm access through small test deposits. Instant verification reduces waiting. Micro-deposits create a fallback path when the bank account cannot be verified instantly through credentials, database validation or direct connection.

Why did my identity verification fail?

Identity verification failed when the system could not connect the applicant, document, account data or risk profile with enough confidence. Common causes include blurry ID photos, poor selfie lighting, expired or damaged documents, name mismatch, address mismatch, outdated records, credit bureau inconsistency, fraud flags and manual review.

Is biometric verification the same as facial recognition?

Biometric verification is not the same as broad facial recognition. For bank onboarding, facial comparison checks whether a live selfie matches the photo on an ID document. Facial recognition is a broader technology category. The practical banking goal is to confirm that the applicant matches the identity document.

Is identity verification mandatory for banks?

Identity verification is mandatory for U.S. banks under customer identification rules tied to CIP, KYC and AML controls. The bank must form a reasonable belief about customer identity before the relationship moves forward. Product risk, account type and institution rules shape the exact verification path.

Final note: identity verification is now part of everyday finance

Identity verification protects account opening, credit decisions, online loans and payment security in digital banking. It is no longer a back-office technical step. Bank identity verification affects how quickly You open an account, link a bank account, apply for a credit card or complete a loan application. Strong verification reduces fraud risk and supports compliance, while mismatched data can create delay, manual review or rejection. Before submitting an application, check Your legal name, address, ID document, phone and email access, and any bank account details You plan to link.